Thanks FedSpeak Giving

AI and NVDA were as always in the headlines last week, but the news was Mr. Williams of the Empire Fed. The Fed is cutting next month.

Long Live the Bernanke Fed

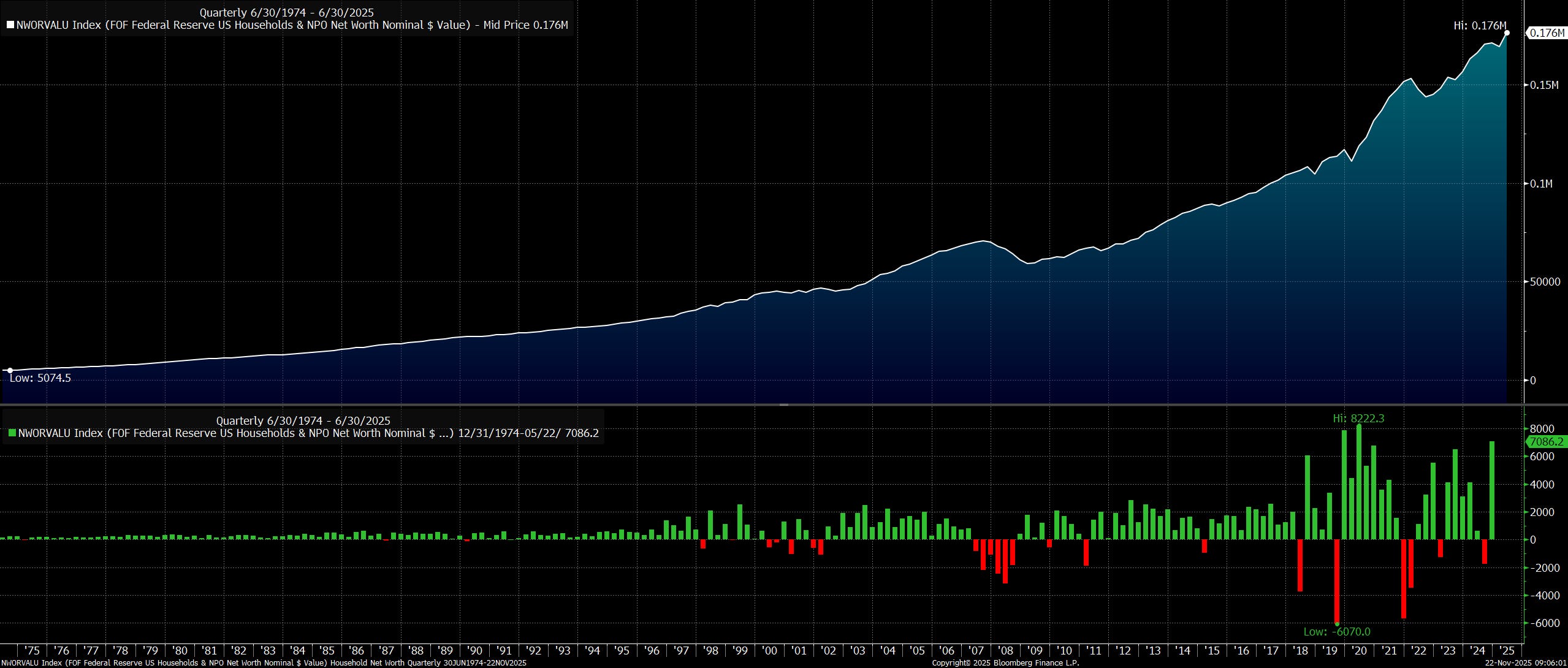

Since the GFC this is the Bernanke Fed: A central bank committed to supporting the wealth effect, mostly a combination of individual stock holdings and single-family residence, motivating individuals to consume more because the value of these and other investments make them feel wealthy. When Bernanke wrote the op ed it sounded like new century voodoo, but it has become the foundation of our socioeconomic structure.

ZIRP, QE, forward guidance, etc. all focus on nominal inflation driven growth supporting ever higher 401K statements and property appraisals, property taxes be damned, fueling wealth transfers from aging parents to their high propensity to consume children and grandchildren while consuming retirement era services.

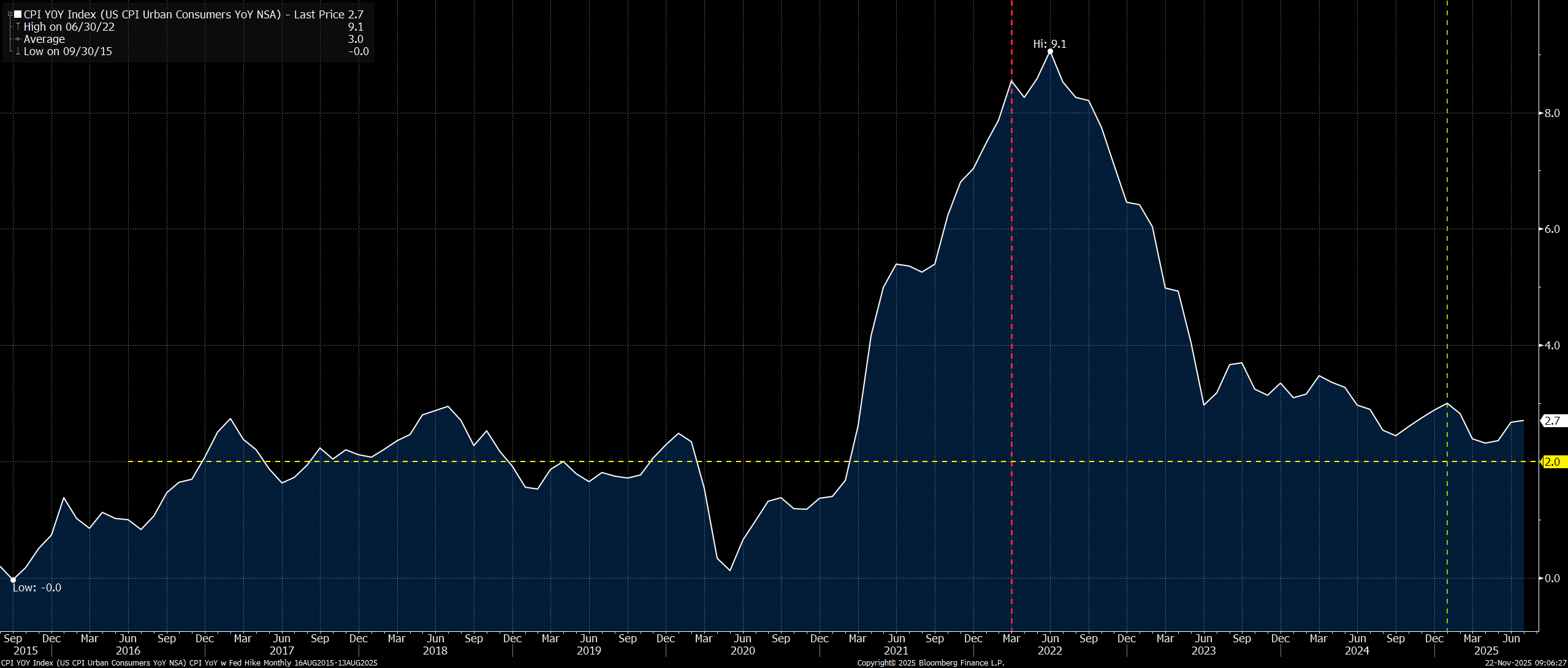

The Bernanke Fed regime was cemented by J. Powell with ill-conceived Average Inflation Targeting (AIT) allowing inflation to run hot, above 2% target so as to average inflation over some period. Powell executed according to plan waiting until CPI YoY was nearly 8% in 2022 before beginning to normalize rates. The Powell led Bernanke Fed post COVID never tightened. It moved swiftly toward neutral and arguably came up short.

The AIT experiment was largely derided though those leading the derision benefit mightily from the folly of AIT.

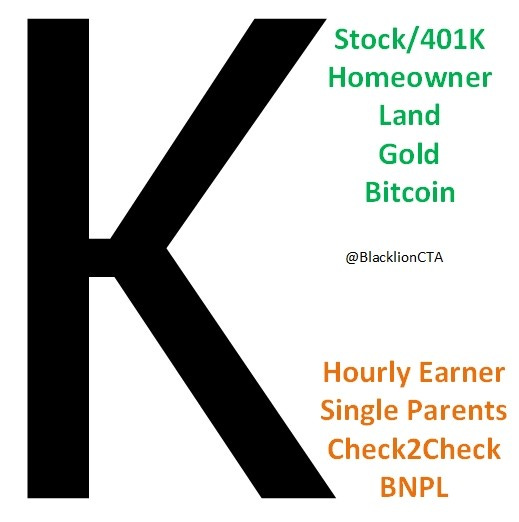

What could go wrong? Turns out folks, especially those without an appreciating single-family residence and fat 401K statement don’t like skyrocketing inflation and start getting feisty at the ballot box installing lifelong big government saviors such as Newsom, Trump, Mamdani, and others.

The week the FOMC began the current cutting cycle Governor Chris Waller, one of the Fed’s thought leaders, a bright gentleman, and finalist to take the helm of the Bernanke Fed from Jerome Powell appeared on CNBC and in more words said the quiet part out loud. The Fed’s big fear is inflation below 2%. The target is now the floor and that is a big political problem in the K Recovery cum K Economy.

The problem: The policy to address the K divide and re-establish 2% as a target requires policy choices that are arguably catastrophic to the tenets of the wealth effect: stocks, homes, other assets save bonds, etc. Specifically, addressing the K divide means abandoning the Bernanke Fed and its treasured wealth effect.

The Fed conducted its semi-official monetary policy review this year and the best they could come up with is some jiggery pokery for ‘run it hot’ not because AIT was a mess, but because nobody in the Eccles building has the spine to disturb the wealth effect.

Jerome Powell’s term expires in May 2026. He is a consensus builder, not a shock and awe guy, and he isn’t going to be a monetary martyr on his way to the country club. For the record I do not believe he serves the balance of his term as governor. J. Powell will be 73 when his term as Chair ends, healthy active bicyclist, rumored net worth $100M+, Grateful Dead fan who misses eating out. There is no personal upside for him remaining at the Fed.

While there isn’t consensus to end the Bernanke Fed regime cracks are emerging with very novel thinking by Lorie Logan, Miki Bowman, real-world banking input from Jeff Schmid, and years of rates experience from Beth Hammack.

The Great FOMC Divide

The FOMC began the current cutting cycle 14 months ago soon pausing a year ago. During the pause a philosophical divide began emerging among FOMC members running contrary to the Fed’s monetary policy regime. Specifically, the regional presidents have become more conservative about easing policy further while the board of governors focuses on growth and labor concerns.

I’ve had numerous personal interactions with the Dallas Fed, other regional presidents and staff, and lesser the governors and their staff. The policy makers and especially their staff are uniformly great listeners and information sponges. All are intellectually curious, and this goes into overdrive at the regional bank level.

Regional Federal Reserve Banks

Regional banks have sizeable community outreach departments, conduct well known manufacturing and service surveys, publish important indexes, etc. and lead with ‘Fed Listen’ events in their districts.

Regional presidents are the first to hear from district businesses what is happening before it shows up in national economic data and even weeks/months before they share it in their own regional indexes, surveys, reports and ultimately the Beige Book. What the regional presidents are hearing is problematic.

I was in the audience for Beth Hammack and Rafael Bostic discussing what they are hearing, and I’ve talked with Lorie Logan’ staff and she recently shared her perspective. All of them are lock step with Jeff Schmid of Kansas City who dissented against cutting rates at the last FOMC meeting.

Inflation is still a big problem

Inflation is minority related to tariffs

This motivated Jeff Schmid to dissent against cutting rates as a recorded voter at the last FOMC. Lorie Logan and Beth Hammack both soft dissented (they aren’t recorded voters this year) and Rafael Bostic entered the meeting reluctant to support a cut and he is non-committal to future cuts.

Other presidents while perhaps not as hawkish as the four I’ve interacted with recently are mostly conservative about near-term cuts.

A key exception is the President of the New York Federal Reserve who has a very unique roll given the additional responsibilities of the NY Fed in the money market, housing the Treasury General Account, and the System Open Market Account (SOMA). The NY Fed President is very influential and, in my view, more akin to the governors than regional presidents.

Board of Governors

The governors including the Chair are more concerned about potential labor market weakness with a good example last week of Verizon announcing 13,000 layoffs.

The board of governors acknowledge inflation greater than 2%, but even after 5 years remain convinced it is trending toward 2%. Mike McKee of Bloomberg challenged Chair Powell on this point at a recent post FOMC presser, and the very relevant and well styled question was side stepped.

The outlier on the board is rookie Steve Miran. Steve is a very smart economist and central banker. There are numerous records of he and I interacting and my complimenting him before he joined the Trump admin. Since he signed the loyalty pledge and surrendered Fed independence with his controversial appointment we’ve not engaged. His positions appear cribbed from Sec. Scott Bessent and POTUS - uber dovish, tone deaf to inflation.

The Fed has a challenging dual (arguably 3) mandate naturally in tension, but their record demonstrates in any conflicts or concerns the majority usually led by the board of governors will prioritize labor and growth and right now growth is inexorably hitched to the wealth effect.

Two Weeks of FedSpeak

The past two weeks of FedSpeak had an interesting demarcation November 10-14 was dominated by regional presidents and this week by governors.

November 10 - 14 Presidents Rumble

This week featured a majority of regional presidents:

Musalem - St. Louis

Collins - Boston

Daly - San Francisco

Hammack - Cleveland

Kashkari - Minneapolis

Schmid - Kansas City

Logan - Dallas

Bostic - Atlanta

There were some governors, Steve Miran of course, speaking, but the presidents made the news and moved the markets with their mostly conservative/hawkish discussions.

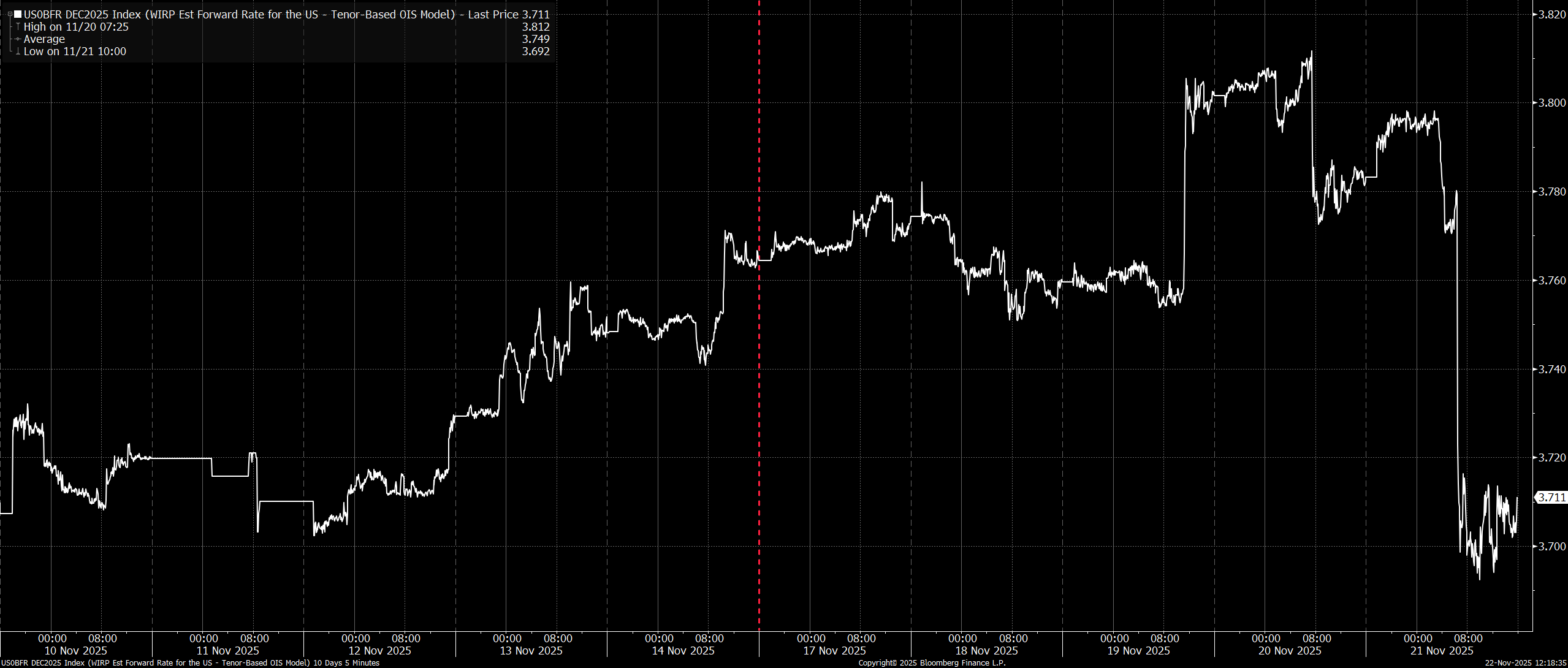

Bloomberg’s World Interest Rate Probability (WIRP) OIS tenor-based model started the week with 62.6% chance of a December cut and ended the week at 43.2%

November 17-21 Governors Strike Back

The week was dominated by the governors more concerned with labor and growth and inclined to cut at the December meeting:

C. Waller

Vice Chair Jefferson

L. Cook

M. Barr

S. Miran

There were several presidents speaking, but their positions were known, did not introduce anything new, and didn’t move the markets much. The emphasis on Monday was Chris Waller, but the real impact was Friday morning.

Previously mentioned the President of the NY Fed occupies a role more akin to a governor and is believed to be very influential inside the committee due to the unique and important functions of the Empire bank. Additionally, the NY Fed President is a permanent FOMC voter and does not rotate with the other regional presidents.

Thursday was a tumultuous day in equity markets and short-term interest rate (STIR) as WIRP OIS odds for a December cut dwindled to 34.9%.

NY Fed President J. Williams spoke in Santiago Chile before Friday’s cash open and issued these key sentences.

I view monetary policy as being modestly restrictive, although somewhat less so than before our recent actions. Therefore, I still see room for a further adjustment in the near term to the target range for the federal funds rate to move the stance of policy closer to the range of neutral, thereby maintaining the balance between the achievement of our two goals.

This was all the market needed to hear. A permanent voter, regional president akin to a governor with the ear of the Chair advocating for the December cut.

The odds for a December cut nearly doubled to more than 60%

The Trade

The trade for the week was expressed in December SOFR futures. Several STIR traders including the occasional STIR speculator author built long SR3Z5 positions during the past two (2) weeks expressing our opinion that the market had become too pessimistic about a December cut. John Williams delivered on Friday morning capping two volatile weeks in STIR markets.

Most will look at this chart and wonder what it is we see. Opportunity for a short-term trade in a perceived offside market with good reward:risk.

Forward Look

The dynamic hasn’t changed. Regional presidents save J. Williams mostly remain cautious on rate cuts influenced by input from their districts while governors have the other side of the trade.

The voters for the final FOMC meeting of 2025

J. Schmid of Kansas City dissented at the previous meeting. A. Goolsbee and A Musalem have both been very conservative in their recent speeches. S. Collins has been neutral/cautious. The remainder have been neutral or supportive of cuts including C. Waller and J. Williams, arguably the most influential of this year’s voters.

The math is that if all the rotating regional presidents dissent and one of the governors dares dissent the majority will still carry the day for a cut.

Jerome Powell is a consensus builder, but more importantly he isn’t a shock and awe monetary martyr.

Additionally, we will not receive any additional impactful e.g. NFP and CPI data before the meeting. The cake is baked in my view - the Fed cuts next month.

Trade ‘Em Straight - Guido

This article is excellent. I completely agree with the final conclusion. Thank you for sharing it.

I’m going to be really honest with you. I think you are going to be Right. I also think that if he does that then he will absolutely end up being remembered as Arthur burns 2.0 which makes zero sense for him legacy wise. Which leads me to my real question.

Do you think he cares more about his legacy right now, or his legacy when people look back in 20 years? Because if he cuts now, in this moment, he is securing Arthur burns status.

Unless the largest recession in quite some time is around the corner (possible) then cutting 3 times into the largest tariffs in 100 years is going to be a hell of a choice.